Seguro de vida:é um investimento inteligente? Compreendendo os fatos

Existem mais de 400.000 agentes de seguros neste país, e quase todos eles adorariam vender a você uma apólice de seguro de vida. Se você comprar uma apólice com prêmios de US$ 40.000 por ano, a comissão normalmente ficaria entre US$ 20.000 e US$ 44.000 para esse agente. Como você pode imaginar, essa comissão pode ser altamente motivadora, especialmente considerando a renda média do agente de seguros de US$ 49.840. Para piorar a situação, muitas das piores políticas oferecem as comissões mais altas. Infelizmente, a grande maioria das apólices vendidas é vendida de forma inadequada e a grande maioria dos que as vendem são vendedores disfarçados de consultores financeiros.

Como resultado deste ridículo conflito de interesses, os agentes podem muitas vezes lançar alguns mitos sérios num esforço para persuadi-lo a comprar o seu produto, o que pode explicar a estatística contundente de que mais de 80% daqueles que compram este produto se livram dele antes da morte e sondagens de médicos reais neste site e no nosso grupo no Facebook mostram que a grande maioria daqueles que compraram apólices de seguro de vida lamentam a sua compra. Se tudo isso é novidade para você, leia Tudo o que você precisa saber sobre seguro de vida antes de continuar com esta postagem.

Embora a maioria dos membros do grupo WCI FB nunca tenha adquirido seguro de vida, daqueles que o fizeram, 76% se arrependem.

Os números são semelhantes, mas ligeiramente inferiores na sondagem em curso neste site (que, ao contrário do grupo FB, permite que a votação seja feita por quem vende estas apólices).

Muitas pessoas pensam que odeio seguro de vida. Na verdade, não. Odeio a forma como é vendido e aqueles que o vendem de forma inadequada. Se você realmente entende como funciona e ainda quer, fique à vontade para comprar o quanto quiser. Isso realmente não me afeta de uma forma ou de outra. Mas estou cansado de encontrar leitores e ouvintes que NÃO entenderam como funcionava quando o compraram e, uma vez que entenderam, NÃO o querem.

Como funciona o seguro de vida

O seguro de vida pode ser configurado de muitas maneiras diferentes, mas, em geral, você paga um prêmio mensal ou anual por um período definido ou até morrer. Quanto maior o período de tempo durante o qual você paga os prêmios, mais baixos serão os prêmios. Sempre que você morre, seu beneficiário recebe o produto da apólice. Uma vez que todas as apólices de vida têm pagamento garantido se você mantê-las até a morte, os prêmios são muito mais altos do que uma apólice de seguro de vida comparável.

Uma apólice de seguro de vida, como outros tipos de seguro de vida permanente, é na verdade um híbrido de seguro e investimento. A apólice acumula valor em dinheiro com o passar dos anos. Esse valor em dinheiro cresce de maneira protegida por impostos, e você pode até pedir dinheiro emprestado sem impostos (mas não sem juros). Após a sua morte, tudo o que você pediu emprestado (mais os juros) é retirado do benefício por morte e o restante é pago ao seu beneficiário. (Você recebe o valor em dinheiro ou o benefício por morte, não ambos.)

Esse aspecto do investimento permite que aqueles que vendem seguros de vida encontrem todos os tipos de motivos criativos para comprá-los e maneiras criativas de estruturá-los. Os defensores mais radicais podem até argumentar que você não precisa de NENHUM outro produto financeiro durante toda a sua vida, já que o seguro de vida aparentemente pode cuidar de todas as suas necessidades, incluindo hipotecas, empréstimos ao consumidor, seguros, investimentos, poupança para faculdade e aposentadoria.

O problema é que, para cada utilização do seguro de vida, geralmente existe uma maneira melhor de lidar com essa questão financeira. Este post apresenta os 38 mitos frequentes sobre seguros de vida propagados por seus defensores.

Mito nº 1 – A vida inteira é ótima para proteção de renda pré-aposentadoria

O seguro de vida não é a melhor maneira de proteger sua renda, mas o seguro de vida é. Antes de se aposentar, você pode adquirir um seguro de vida barato para cuidar de seus entes queridos em caso de morte prematura. Uma apólice de seguro de vida com prêmio de nível de 30 anos com valor nominal de US$ 1 milhão, comprada para uma pessoa saudável de 30 anos, custa US$ 680 por ano. Uma apólice vitalícia semelhante custará mais de 10 vezes mais, de US$ 8.000 a US$ 10.000 por ano. É dinheiro que não pode ser gasto no pagamento de hipotecas ou férias, nem investido na aposentadoria.

Mito nº 2 – A vida inteira é a melhor maneira de obter um benefício permanente por morte

A vida inteira não é a melhor maneira de obter um benefício permanente por morte – a vida universal garantida e sem lapso é. Existem algumas pessoas selecionadas que precisam ou desejam uma apólice de seguro que será paga no momento da morte, quando for o caso. Isso pode ser útil para alguns problemas incomuns de planejamento imobiliário. No entanto, existe um produto melhor que oferece isso e é muito mais barato que o seguro de vida. É chamado de Seguro de vida universal garantido e sem caducidade . NÃO acumula nenhum valor em dinheiro, mas simplesmente fornece um benefício vitalício por morte. Custa apenas a metade do seguro de vida, então você não ficará surpreso ao saber que a comissão do agente nesta venda será muito menor.

Chame-me de cínico, mas suspeito que essa possa ser uma das razões pelas quais você nunca ouviu falar de vida universal garantida e sem lapso. O seguro de vida oferece um benefício de morte garantido que é PROJETADO (mas não garantido) para crescer lentamente, de modo que, se você morrer dentro de sua expectativa de vida ou mais tarde, deixará para trás um pouco mais do que o benefício de morte da apólice original.

Benefícios por morte e inflação

Uma apólice vitalícia que examinei recentemente projetou que o benefício por morte de uma apólice de US$ 1 milhão, comprada aos 30 anos, seria de US$ 3,17 milhões na morte aos 83 anos. Isso parece ótimo, quase como uma proteção contra a inflação do benefício por morte. Exceto que a inflação histórica é algo em torno de 3,1%. Com 3,1%, 1 milhão de dólares agora equivaleria a 5,04 milhões de dólares daqui a 53 anos. Uma política vitalícia seria devastada por uma inflação inesperada, uma vez que os dividendos são garantidos principalmente por obrigações nominais, cujos valores seriam assassinados num ambiente de inflação elevada.

Portanto, o seguro de vida não é a melhor forma de fornecer um benefício nominal garantido por morte vitalícia nem um benefício real garantido por morte vitalícia. Então, para que serve? Que tal um benefício garantido por morte que pode aumentar se a seguradora desejar aumentá-lo? Você estaria disposto a pagar prêmios duas vezes mais altos por isso? Eu não pensei assim.

Mito nº 3 – Seguro de vida oferece um ótimo retorno de investimento

A vida inteira não é a melhor maneira de investir – os investimentos tradicionais são. Quando você paga os prêmios de vida inteira, parte do dinheiro vai para a compra de seguro, parte vai para despesas gerais e lucros da seguradora e parte vai para a comissão do vendedor. O restante vai para a parte do valor em dinheiro da apólice.

A cada ano, a seguradora declara um dividendo, e se houver $ 10.000 na parcela do valor em dinheiro e o dividendo for de 6%, então $ 600 serão creditados em seu valor em dinheiro. O dividendo é aplicado apenas ao valor em dinheiro, não ao prêmio total pago, portanto, a taxa média de dividendos não está de forma alguma relacionada ao retorno real da apólice como um investimento. Na verdade, o retorno do investimento é geralmente negativo durante pelo menos uma década. Analisei recentemente uma política para um homem saudável de 30 anos com uma esperança de vida de 53 anos. O retorno garantido sobre o valor em dinheiro foi inferior a 2% ao ano APÓS 5 DÉCADAS .

Mesmo se você usar os valores “projetados” otimistas da seguradora, ainda estará prevendo um retorno inferior a 5%. Na realidade, você provavelmente obterá um retorno de 3% a 4%. Considerando que você terá que manter esse “investimento” por 5 décadas, isso não parece ser uma grande compensação. Se você tem décadas para investir, é muito mais sensato assumir mais riscos com seus investimentos e obter um retorno maior. É provável que um investimento em ações ou imóveis proporcione um retorno ao longo de décadas na faixa de 7% a 12%. US$ 100.000 investidos por 50 anos a 3% ao ano se transformarão em US$ 438.000. Se crescer 9%, você acabará com US$ 7,4 milhões, ou 17 vezes mais dinheiro. A taxa na qual você compõe seus investimentos de longo prazo é importante, especialmente durante longos períodos de tempo.

Mito nº 4 – As seguradoras são grandes investidores

Alguns agentes acreditam que as companhias de seguros podem, de alguma forma, obter retornos de investimento que você ou eu não conseguimos encontrar em outro lugar e repassar esses grandes retornos aos seus titulares de apólices. Pode ser esclarecedor olhar nos bastidores e ver o que realmente está no portfólio de uma seguradora. Em 2016, os activos das companhias de seguros foram investidos 67% em obrigações (quase todas em obrigações corporativas e do tesouro comuns), 1% em acções preferenciais, 12% em acções ordinárias, 8% em hipotecas, 1% em imobiliário, 4% em dinheiro, 2% em empréstimos aos seus titulares de apólices e cerca de 5% em “outros”. Graças à revolução dos fundos de índice, um investidor individual pode comprar quase tudo isso por menos de 10 pontos base por ano em despesas. A gestão ativa não funciona melhor para as companhias de seguros do que para os fundos mútuos.

Como seria de esperar, os retornos de uma carteira composta principalmente por títulos do tesouro (atualmente rendem 1%-2%) e títulos corporativos (atualmente rendem 3%-4%) não são particularmente elevados. Então, de onde vêm os dividendos? Parte vem do retorno da carteira de investimentos, parte vem das taxas daqueles que desistiram de suas apólices, e parte vem de “créditos de mortalidade”, que é basicamente dinheiro que eles não tiveram que pagar aos beneficiários porque menos pessoas morreram do que o planejado (ou seja, você pagou demais pela parte do seguro da apólice devido a regulamentações estaduais). Não existem investimentos mágicos em que as seguradoras possam investir e que você não possa investir sem a empresa. Cada camada adicional entre você e o investimento apenas aumenta as despesas e diminui os retornos.

Mito nº 5 – A vida inteira é uma grande classe de ativos

Existem muitas classes de ativos que vale a pena incluir em um portfólio diversificado, mas a vida inteira não é uma delas. Os vendedores de seguros geralmente recorrem a esse argumento quando percebem que não conseguem convencê-lo de que a vida inteira é um grande investimento por si só. Dizem que se você misturar isso em uma carteira de ações, títulos e imóveis, isso melhorará a carteira geral. No entanto, você pode chamar o que quiser de classe de ativos. O esterco de cavalo pode ser uma classe de ativos, mas isso não significa que você deva investir nele. Pense desta forma. Se eu te dissesse que tenho uma classe de ativos com as seguintes características:

- 50% de carga inicial no primeiro ano

- Penalidades de renúncia que duram anos

- Requer contribuições contínuas por décadas

- Difícil reequilibrar com outras classes de ativos

- Apoiado pelas garantias de uma única empresa (e tudo o que você puder obter de uma associação de garantia estatal)

- Exige que você pague juros para receber seu dinheiro

- Retornos negativos garantidos para a primeira década

- Retornos baixos, mesmo que você o mantenha por décadas

- Deve ser mantido por toda a vida para proporcionar um retorno de investimento ainda que baixo

- Excluído do investimento por problemas de saúde ou hobbies perigosos

você compraria? Claro que não.

Mito nº 6 – A vida inteira é uma ótima maneira de economizar impostos

A vida inteira não é a melhor maneira de reduzir sua conta de impostos sobre investimentos, mas as contas de aposentadoria são. Muitos agentes gostam de elogiar os benefícios fiscais do seguro de vida, muitas vezes comparando-o a um 401 (k) ou a um Roth IRA. O valor em dinheiro cresce de maneira protegida por impostos, o valor em dinheiro pode ser emprestado sem impostos e os rendimentos da apólice no momento da sua morte são isentos de impostos sobre renda (embora não sobre bens). Portanto, alguns defensores da vida inteira sugerem que você use um seguro de vida em vez de uma conta de aposentadoria como 401 (k) ou Roth IRA. No entanto, um 401(k) ou Roth IRA não só proporciona MAIS poupança fiscal e permite-lhe investir em investimentos mais arriscados que provavelmente lhe proporcionarão um retorno mais elevado, mas também não tem de pedir emprestado o seu próprio dinheiro, nem pagar juros pelo privilégio de o fazer.

Publiquei anteriormente sobre as três maneiras pelas quais um 401 (k) economiza impostos e como o seguro de vida inteira não é como um Roth IRA. Também postei sobre como os investimentos com eficiência fiscal em uma conta de investimento tributável não carregam quase a carga tributária que os agentes gostam de dizer que carregam. Existem benefícios fiscais em investir em seguro de vida? Sim, mas eles estão dramaticamente exagerados.

Mito nº 7 – O seguro de vida protege seu dinheiro dos credores

Os corretores de seguros adoram usar isso com médicos, que podem ficar paranóicos com questões de proteção de ativos. No entanto, muitas vezes não mencionam (ou talvez nem saibam) que as leis de proteção de ativos são muito específicas de cada estado. Por exemplo [2022] , no Alabama, apenas US$ 500 do valor em dinheiro do seguro de vida estão protegidos dos credores, mas 100% do dinheiro em seu 401 (k) ou IRA está protegido. West Virginia oferece proteção de apenas US$ 8.000. A Carolina do Sul protege US$ 4.000. New Hampshire não oferece nenhuma proteção. Muitos estados oferecem 100% de proteção para o valor em dinheiro do seguro de vida, mas você provavelmente deveria consultar as leis específicas do seu estado antes de cair nesse mito.

Mito nº 8 – Você precisa de uma vida inteira para planejar o patrimônio

O seguro de vida com valor monetário tem alguns excelentes recursos de planejamento imobiliário que podem ser muito úteis. No entanto, a grande maioria das pessoas, incluindo os médicos, não precisa desses recursos. O principal benefício do seguro de vida é que você recebe muito dinheiro livre de imposto de renda quando morre. Isso pode ajudar com muitos problemas de liquidez, como a propriedade de uma propriedade cara ou um negócio privado. Se você tem dois filhos que deseja dividir igualmente em sua propriedade, e a maior parte de sua propriedade é uma fazenda familiar, eles teriam que vender a fazenda, cortá-la ao meio ou fazer com que um comprasse o outro para compartilhar igualmente. Porém, se você também tivesse uma apólice de seguro de vida com o mesmo valor da fazenda, uma criança poderia ficar com a fazenda e a outra poderia ficar com o produto do seguro. Da mesma forma, no feliz caso de você ter um patrimônio muito grande (mais de US$ 5 milhões para pessoas solteiras no código tributário federal, mas pode ser muito menor em alguns estados), os rendimentos do seguro de vida podem ser usados para pagar os impostos sobre o patrimônio. Isto seria útil mesmo com um único herdeiro para evitar que ele vendesse uma propriedade ou negócio valioso a preços de liquidação para pagar a conta do imposto.

Algumas pessoas também gostam de colocar o seguro de vida dentro de um fundo irrevogável para diminuir o tamanho de seus bens e evitar impostos sobre heranças. Embora você possa colocar investimentos tributáveis simples no trust (e provavelmente sairia bem devido a retornos mais elevados), as taxas de imposto do trust podem ser bastante altas, prejudicando seriamente os retornos de investimentos ineficientes em termos fiscais, para não mencionar o fator incômodo. É importante ressaltar que não é o seguro de vida que economiza dinheiro em impostos imobiliários, é o fato de você estar doando seus bens antes de morrer, colocando-os no fundo fiduciário.

Contudo, o facto é que a grande maioria dos americanos, mesmo os médicos, e mesmo incluindo os médicos com um “problema de imposto sobre o património”, não precisam de seguro de vida para fazer um planeamento patrimonial eficaz. A maioria das pessoas morrerá sem qualquer carga tributária imobiliária. Daqueles cujas propriedades deverão alguns impostos sobre a propriedade, a grande maioria possui ativos líquidos que podem ser usados para pagar os impostos. Mesmo se você quiser reduzir o tamanho de seu patrimônio para evitar impostos sobre heranças, poderá fazê-lo facilmente sem adquirir um seguro de vida. Você e seu cônjuge podem doar US$ 16.000 cada [2022 — visite nossa página de números anuais para obter os números mais atualizados] a qualquer herdeiro em qualquer ano, sem quaisquer implicações fiscais sobre heranças/doações. Por exemplo, se você tivesse 4 filhos e cada um deles tivesse 4 filhos e todos os 20 herdeiros fossem casados, seriam 40 pessoas. 40 x US$ 16 mil x 2 =US$ 1,28 milhão por ano que pode ser retirado de sua propriedade sem pagar nenhum imposto sobre herança/doações. Não demorará muito para ficar abaixo do limite do imposto imobiliário nessa taxa, não é necessário seguro.

Mito nº 9 – A vida inteira é uma ótima maneira de pagar a faculdade

Alguns agentes chegam ao ponto de sugerir que você use uma apólice vitalícia para pagar a faculdade de seus filhos. Você pode fazer isso? Claro. Você simplesmente contrai empréstimos e envia esse dinheiro para a universidade para pagar as mensalidades. Mas é melhor economizar para a faculdade usando um bom 529 por vários motivos. Primeiro, muitas vezes você obtém uma redução de impostos estaduais usando um 529 que não está disponível para seguro de vida. Em segundo lugar, você não precisa pedir dinheiro emprestado ao seu 529, basta retirá-lo. Não é necessário pagamento de juros. Por último, mas certamente não menos importante, considere o prazo para economizar na faculdade. Os pais geralmente economizam para a faculdade durante um período de 5 a 20 anos. Ao investir esse dinheiro de forma agressiva, eles podem esperar um retorno de 7% a 10%. O seguro de vida tem retornos muito baixos para períodos inferiores a 20 anos. Na verdade, muitas vezes o retorno do valor em dinheiro do seu “investimento” durante toda a vida é negativo durante pelo menos uma década. É importante garantir que seu dinheiro trabalhe tanto quanto você e que esteja de férias durante a primeira década de uma apólice vitalícia. Os defensores da vida inteira apontarão que, se você morresse, o benefício por morte ainda poderia pagar a faculdade do Junior, mas é muito mais barato cobrir esse risco com seguro de vida.

Mito nº 10 – A vida inteira é um luxo que você deseja

Os agentes de seguros ocasionalmente recorrerão a esse argumento quando for apontado que um cliente não tem realmente qualquer tipo de necessidade de um benefício permanente por morte. Eles admitem que o cliente na verdade não precisa de seguro de vida. Em seguida, tentam vendê-lo com base no fato de tê-lo como símbolo de status ou luxo. “Claro, você não precisa disso, é um luxo.” Um luxo é, por definição, algo que você não precisa. Prefiro que meus luxos sejam algo que eu realmente goste. Portanto, antes de comprar um seguro de vida como um luxo, pergunte-se:“O que eu realmente gosto?” Se for possuir seguro de vida, tudo bem, compre algum. Mas aposto que a maioria de nós preferiria um luxo como um belo carro, um cruzeiro com os netos ou talvez uma doação para uma instituição de caridade favorita.

Mito nº 11 – A vida inteira permite que você gaste seus outros bens, proporcionando flexibilidade valiosa na aposentadoria

A vida inteira não é a melhor maneira de garantir que você não fique sem dinheiro; anuizar alguns de seus ativos é. A vida inteira não é a melhor maneira de lidar com a questão do segundo a morrer, mas estruturar adequadamente as pensões e anuidades é. Os agentes vitalícios gostam de propor cenários de aposentadoria que façam você sentir que precisa ou pelo menos deseja ter um seguro de vida permanente, especialmente para um casal. Por exemplo, falarão sobre uma pensão que só é paga até a morte do cônjuge que trabalha. Ou falarão em anuizar alguma parte de seus bens com base na vida de apenas um membro do casal. Em seguida, eles sugerirão que o produto da apólice de seguro de vida seja usado para despesas de subsistência do segundo cônjuge falecido. Não há razão para usar uma apólice vitalícia desta forma. Se você deseja que sua pensão dure até a morte de ambos, selecione essa opção. Se você deseja que sua anuidade dure até a morte de ambos, escolha essa opção. Sim, o pagamento será a uma percentagem ligeiramente inferior, mas a diferença entre os pagamentos é inferior ao custo de uma apólice de seguro de vida que cobriria a perda dessa pensão. Simplesmente não é a solução certa para o problema. O seguro de vida oferece alguma flexibilidade na aposentadoria? Claro, mas o custo dessa flexibilidade é muito alto.

Mito nº 12 – A vida inteira é uma ótima maneira de comprar coisas caras

A vida inteira não é a melhor maneira de comprar coisas caras, economizar para isso é. Existem alguns vendedores de seguros realmente criativos que defendem sistemas como o Bank on Yourself ou o Infinite Banking. O esquema básico é este:ao estruturar sua apólice adequadamente com acréscimos pagos, você obtém muito valor em dinheiro em sua apólice nos primeiros anos, de modo que atinge o ponto de equilíbrio em 3-4 anos, em vez de 8-15 anos. Você também compra uma apólice que é “reconhecimento não direto”. Isso significa que quando você toma um empréstimo da apólice, a seguradora continua a pagar dividendos sobre o valor que estava lá antes de você emprestá-lo, de modo que os dividendos da apólice cancelam essencialmente os pagamentos de juros devidos sobre o empréstimo. Agora, em vez de ir à sua conta poupança ou a um banco para pedir dinheiro emprestado quando precisar de um carro, uma geladeira ou uma propriedade para investimento, você toma emprestado de sua apólice vitalícia, essencialmente sem nenhum custo. Além disso, o valor em dinheiro da apólice que você não toma emprestado crescerá mais rápido do que o dinheiro em um banco de poupança.

Então qual é o problema? O problema é que você tem que comprar uma apólice vitalícia de que não precisa. Você pode atingir o ponto de equilíbrio mais cedo do que faria com uma política tradicional, mas ainda há vários anos de retornos negativos e, no longo prazo, os mesmos retornos baixos. É melhor ganhar 4%-5% ao ano após 5 anos ou ganhar 1% ao ano a partir do ano 1? Bem, durante os primeiros 6 ou 7 anos, você estará melhor com a conta poupança de 1% ao ano. Além disso, se as taxas de juros subirem desde seus mínimos históricos, você ainda ficará preso a esse sistema pelo resto da vida. Não faz muito tempo que eu conseguia obter mais de 5% de um fundo do mercado monetário. Também parece ser muito fácil financiar um carro em uma concessionária com taxas de juros extremamente baixas. 0% ou 1% não são incomuns. É melhor você pedir emprestado a eles a 1% do que a sua apólice a 5%. É um problema semelhante com eletrodomésticos e hipotecas. Você faz todo esse esforço para poder pedir emprestado a si mesmo e depois percebe que é mais barato pedir emprestado a outra pessoa. Por fim, se você não precisar fazer uma compra por 5 ou 10 anos, terá tempo para investir em algo que provavelmente terá um retorno muito maior do que uma apólice vitalícia. Aqueles que apostam em si mesmos estão sendo enganados? Não necessariamente, mas geralmente eles exageram nos benefícios de seu esquema. Seus defensores são principalmente agentes de seguros que buscam aumentar as vendas por meio de marketing criativo. Economizar é simplesmente a melhor maneira de fazer grandes compras do que comprar uma apólice vitalícia.

Mito nº 13 – Pessoas ou empresas realmente ricas compram seguro de vida para toda a vida, então você também deveria fazer isso

Os defensores da vida inteira, especialmente aqueles que defendem o uso de sua apólice como banco, gostam de ressaltar que muitas pessoas muito ricas e muitas empresas (incluindo bancos) na verdade compram seguro de vida inteira. Embora seja verdade, é irrelevante para a pessoa típica. As grandes empresas não têm acesso às opções de contas de aposentadoria com economia de impostos que um indivíduo de classe média tem. Indivíduos ultra-ricos já atingiram o limite máximo. Quando você tem muito mais dinheiro do que precisa, o retorno do seu dinheiro não importa tanto. Bill Gates pode investir em algo que proporcione retornos de 2% a 5% porque ele não precisa de seu dinheiro para trabalhar muito. Isso simplesmente não é verdade para a grande maioria das pessoas das classes média e alta, incluindo os médicos. Conforme discutido acima, as pessoas ultra-ricas também aproveitam mais os benefícios limitados de planejamento patrimonial e de proteção de ativos do seguro de vida permanente. Em suma, os baixos retornos inerentes a toda a vida são um problema muito menor para eles do que para você.

Mito nº 14 – Você deve comprar a vida inteira quando for jovem

Os vendedores de toda a vida gostam de salientar que a vida inteira é muito mais barata se você a comprar quando for jovem. Embora seja verdade que os prêmios são mais baixos se você comprar uma apólice aos 25 anos do que se você a comprar aos 55, uma vez levado em conta o valor do dinheiro no tempo e o fato de que você pagará os prêmios por mais 3 décadas, não é um investimento melhor em uma idade jovem do que em uma idade mais avançada. Os atuários são pessoas muito inteligentes e, para um risco relativamente fácil de modelar, como a morte, podem precificar o seguro com bastante eficiência.

Além dos prêmios mais baixos, há duas outras razões pelas quais parece melhor comprá-lo quando você é jovem. Primeiro, essa comissão é distribuída por mais anos, por isso tem menos impacto nos seus retornos globais. Mas a alternativa de não pagar a comissão é muito mais atraente. Em segundo lugar, é possível que você se torne menos saudável ou pratique algum esporte perigoso mais tarde na vida. Esta é uma das sérias desvantagens de usar o seguro de vida como investimento – nem todos podem usá-lo. Ou eles não se qualificam para isso ou o preço do seguro é tão alto que o retorno do investimento é ainda menor do que seria de outra forma. Não vejo isso como uma razão para comprá-lo quando você é jovem, vejo isso como uma razão para não comprá-lo. Você pode imaginar se a Vanguard enviasse um paramédico à sua casa para tirar sangue antes de permitir que você comprasse o fundo S&P 500?

Mito nº 15 – Isenção de passageiros premium é uma boa maneira de proteger sua aposentadoria por invalidez

O seguro de vida não é a melhor maneira de proteger sua renda de aposentadoria contra invalidez, mas o seguro de invalidez. Reconhecendo que os prêmios de seguro de vida são muito caros e seriam difíceis de pagar em caso de invalidez, as seguradoras passaram a oferecer um passageiro que renunciaria aos prêmios em caso de invalidez. Às vezes você nem parece ter que pagar a mais por esse benefício. Aqueles que caem nessa tática perdem alguns pontos. Primeiro, as garantias não são gratuitas. Cada garantia custa-lhe dinheiro na forma de um retorno menor, quer a seguradora cobre mais pela garantia ou “incorpore-a na apólice” para que fique oculta.

Em segundo lugar, o seguro de invalidez é complicado e a definição de invalidez é muito importante. A maioria dos médicos que desejam cobertura de invalidez gastam muito dinheiro para obter uma apólice realmente boa com uma definição ampla de deficiência, incluindo cobertura de “ocupação própria”, porque querem ter certeza de que a empresa terá que pagar no caso de sua invalidez. Os passageiros vendidos em apólices vitalícias não são tão abrangentes e têm muito menos probabilidade de serem pagos nas muitas áreas cinzentas em que as deficiências costumam cair. É quase certo que será melhor comprar uma apólice de invalidez maior, em vez de uma isenção vitalícia do passageiro premium. Seu seguro de invalidez também pode oferecer um passageiro de proteção de aposentadoria. Embora também tenham problemas (principalmente na forma como o benefício é pago), são melhores do que tentar obter seu seguro de invalidez com uma apólice de seguro de vida.

Se você está planejando uma aposentadoria antecipada como eu, você pode perceber que não precisa de sua cobertura de invalidez para proteger suas contribuições para a aposentadoria, pelo menos depois de alguns anos de grandes economias. Considere ter um portfólio de US$ 750 mil aos 40 anos. Você calcula que precisa de US$ 2 milhões em dólares de hoje para a aposentadoria. Você planeja economizar muito para conseguir isso aos 50 anos e se aposentar. Qual é o plano alternativo se você ficar incapacitado e não conseguir economizar todo esse dinheiro? Seu seguro de invalidez não paga apenas até os 50 anos. Ele paga até os 65 anos. Portanto, você não precisa de sua carteira para cobrir esses 15 anos. Você também pode começar a receber pagamentos da Previdência Social quando os pagamentos por invalidez terminarem. Como você não precisa mexer no seu portfólio, ele pode continuar a crescer. Se crescer 5% após a inflação, quando você atingir os 65 anos valerá mais de US$ 2,5 milhões em dólares de hoje. Não compre um seguro que você não precisa. Mas mesmo antes de você ter qualquer tipo de carteira, a melhor maneira de proteger suas economias para a aposentadoria é comprar MAIS seguro de invalidez, e não tentar obtê-lo com uma apólice de vida inteira. Mesmo que você pudesse usar a cobertura extra para fornecer sua carteira de aposentadoria, você precisa ser capaz de colocá-la em um investimento com alto retorno, que é improvável que a vida inteira proporcione. Uma conta tributável investida agressivamente é adequada, uma vez que sua renda principal, se for deficiente, seus benefícios de seguro de invalidez, são isentos de impostos.

Mito nº 16 - Você deve trocar sua péssima apólice de vida inteira por uma nova e brilhante

Como um agente recebe uma nova comissão cada vez que vende uma nova apólice, mesmo que substitua uma antiga da mesma empresa, ele tem um sério conflito de interesses ao fazer recomendações a você. Eu interajo com muitos corretores de seguros neste blog e nenhum deles concorda com os outros sobre o que é uma apólice de seguro de vida “adequadamente estruturada”. Isso significa que se você procurar um segundo agente, ele quase certamente lhe dirá que existe uma maneira melhor de fazer isso. Contudo, para que valha a pena trocar uma política por outra, a política original tem de ser absolutamente horrível, especialmente depois de algumas décadas. A razão para isto é que os baixos retornos do seguro de vida estão concentrados nos primeiros anos. Dei uma olhada em uma política recentemente. Este foi configurado como um investimento com acréscimos integralizados para os primeiros 25 anos. Foi a melhor tentativa do agente de maximizar os retornos de uma apólice. Esta é a aparência dos retornos anualizados:

Garantido Projetado Primeiros 10 anos - 1,84%0,98%Próximos 15 anos2,55%5,47%Próximos 25 anos1,99%5,13%

Isto demonstra que os baixos retornos estão altamente concentrados nos primeiros anos. Com esta política específica, os retornos diminuem após 25 anos, porque é quando você para de fazer acréscimos pagos. Com uma política mais tradicional, a terceira linha seria ligeiramente superior à segunda linha. Mas a moral da história é que se deve comprar primeiro a “política certa”, e mesmo uma política de baixa qualidade com mais de 10 anos será melhor do que uma política totalmente nova e melhor. Esta é também a razão pela qual pode ser uma boa ideia manter uma apólice vitalícia mais antiga, mesmo que comprá-la tenha sido um erro. Também é digno de nota ver quão pouco risco a seguradora está realmente assumindo, já que nem sequer garante que o seu valor em dinheiro acompanhará a inflação.

Mito nº 17 – A vida inteira é a única maneira de repassar dinheiro aos herdeiros sem imposto de renda

A vida inteira não é a única maneira de repassar dinheiro aos herdeiros sem imposto de renda após sua morte. Na verdade, nem é a melhor maneira, é um Roth IRA. Quando você morre, seus herdeiros recebem um benefício de seguro por morte isento de imposto de renda. O que os agentes muitas vezes deixam de mencionar é que quase tudo que seus herdeiros recebem de você quando você morre é isento de imposto de renda. Graças ao aumento da base no momento da morte, qualquer coisa fora de uma conta de aposentadoria, incluindo móveis, automóveis, ações, dinheiro, fundos mútuos e imóveis, é reavaliada no dia da sua morte. Como a base agora é igual ao valor, não há impostos sobre ganhos de capital devidos. Herdar uma conta de aposentadoria pode ser ainda melhor, especialmente uma conta Roth onde os impostos já foram pagos. Você pode retirar todo o dinheiro no mesmo ano em que o herdou e não pagar nenhum imposto. Ou você pode “esticar”, fazendo retiradas gradualmente ao longo de décadas até morrer. Enquanto isso, continua a crescer sem impostos. You can stretch an inherited tax-deferred account too, but you do have to pay taxes on any money withdrawn from the account.

Myth #18 — With Whole Life, There Is No Way I Can Lose Money

People invest in whole life insurance because they like guarantees. The insurance company guarantees that you'll get a certain rate of growth on your investment and it guarantees a death benefit. The guarantees, however, aren't worth nearly as much as people often assume. For instance, the guaranteed scale of any whole life insurance policy guarantees that your money will grow slower than the historical rate of inflation, despite sticking with it for half a century. Before deciding to trust a single company with your life savings, you might want to consider what happens if it goes out of business. There are state insurance guarantee associations that will cover the cash value and death benefit of your policy, but how much will they really cover? You might be surprised how little it is. In my state, only $500K in death benefit and $200K in cash value is covered, NO MATTER HOW MANY POLICIES YOU OWN. Your state is probably similar. No wonder agents are always talking about the long-term viability of their insurance company. It really does matter! Now I don't think the risk of any given insurance company going out of business in any given year is very high, nor do I think a typical purchaser is likely to end up with exactly the guaranteed growth rate. But before buying, you should realize that investing in whole life insurance isn't the risk free proposition agents like to present it as.

Myth #19 — Life Insurance Should Not Be “Rented”

This one is pretty easy to see through, but you still see agents using it frequently. Since everyone “knows” that it is better to own a home than rent one, the agent says something like “You wouldn't rent your home for the rest of your life would you? So why would you rent your life insurance?” Basically, the agent is referring to the fact that if you use term insurance after age 60 or so, it becomes more and more expensive each year, just like renting a home. But unlike a home, you don't need life insurance after you become financially independent. When you only need a home for a year or two or three, it is a better idea to rent than to buy. When you only need life insurance for a decade or two or three, it is also a better idea to “rent” than to buy. The opportunity cost of “ownership” is simply too high.

Myth #20 — Banks Own Life Insurance So You Should Too

This is a frequent one heard from the Bank on Yourself/Infinite Banking crowd. An underpinning of this school of thought is that the greedy banks are taking over the world so you should only do your financial work through the trustworthy insurance companies. To be honest, I don't have massive distrust for either one of these industries. Both industries have mutually-owned options (mutual life insurance companies and credit unions) where, like Vanguard, the customers own the company. The agents like to point out that banks actually own whole life insurance as part of their “Tier One Capital,” the money used to determine if the bank is adequately capitalized or not. This is somehow to make you fear that the banks know something you don't, like the financial world is about to implode and any of those using banks instead of insurance companies for their financial needs are going to go broke. Tier One Capital is a measure of a bank's financial strength. Banks use less than 25% of their Tier One Capital to buy single premium whole or universal life insurance on a group of employees. The bank owns the policy and is the beneficiary. When the employee keels over, the bank gets the cash. The bank is buying the policy primarily for the death benefit, not because the return is particularly high.

Tier One Capital is highly regulated and it is difficult for a bank to include riskier assets such as common stock(aside from that of the bank, which makes up most of Tier One Capital) and REITs in its Tier One Capital. When you are stuck choosing between low-risk/low-return investments, then you can understand why a bank might consider something like cash value life insurance with part of that money. However, individual physician investors investing for retirement have fewer restrictions on their investment options for their retirement. Most of them have significant need for their retirement money to grow. The returns available with cash value life insurance generally are not high enough for them to reach their goals. Even so, consider what a bank does with most of its Tier One Capital—it buys the only stock it can, it's own. If whole life insurance was so awesome, you'd think the bank would use all of its Tier One reserves to buy it. In short, doctors aren't banks, so doing what banks do isn't necessarily smart. Tier One Capital is highly regulated and it is difficult for a bank to include riskier assets such as common stock.

Myth #21 — Corporate CEOs Own Whole Life Insurance So You Should Too

Agents, particularly of the Bank on Yourself type, love to point out that the golden parachutes for many highly-paid CEOs include cash value life insurance policies. However, just as the financial situation of a bank is dissimilar from that of a physician, so is the financial situation of a CEO making $10 Million a year different from that of a physician. When you're making a gazillion dollars a year, rate of return on your money becomes much less important and thus the benefits of whole life (asset protection, tax, estate planning, etc.) become relatively more important. It isn't that returns on whole life magically get better. Again, if you are in a position that you only need your long-term money to grow at 3%-5% nominal per year, then feel free to invest in whole life insurance. Most of us, however, need higher growth. Remember that a doctor making $200,000 per year and a CEO making $10 Million per year are in very different financial circumstances and what works fine for one will not necessarily work well for the other.

Myth #22 — Banks Failed During The Great Depression, But Insurance Companies Didn't

This myth again preys on the fears of a global economic meltdown. In 1933 there were two holidays. The first was a “Banking Holiday” in which the banks were closed for 10 days as sweeping regulatory changes took place. The second was an “Insurance Holiday” in which for a period of nearly six months you could neither surrender your cash value life insurance policies for cash, nor borrow against them. Aside from this holiday, 14% (63 companies) of life insurance companies actually DID fail during The Great Depression. In fact, if they would have actually marked to market the bonds and mortgages they held, they would have ALL been insolvent. Reforms were put in place during The Great Depression that fixed many of the problems leading to bank failures and the banking holiday. However, these reforms were never put in place for insurance companies.

Myth #23 — After-Tax, Whole Life Returns Are Better Than Bond Returns

This one usually goes like this. “If you can buy a bond yielding 5% and are in a 45% marginal tax bracket, the after-tax yield on that is just 2.75%. A whole life policy with a “tax-free” internal rate of return of 5% is better.” This is an apples to oranges comparison. What is the 1 year return on that whole life policy? 2.75% sounds a whole lot better to me than a -50%. Even at 10-20 years, the bond is still way ahead.

I wrote about a physician who was pleased with his 7% return on his whole life policy bought in 1983 (don't expect to see that again any time soon). Except that he could have bought a 30-year treasury that year yielding 10.5%. 10 years later, as his whole life policy is breaking even and interest rates have dropped, the bond purchaser has not only already more than doubled his money just from the coupon payments, but the capital gains on that bond added another 50% to his return. That investor would have done even better purchasing equities in 1983, the start of an 18 year bull market. A bond, which can be sold any day the market is open, simply cannot be compared in any fair manner to an insurance policy which must be held for life to have any decent kind of return. Besides, most physician investors can hold taxable bonds inside retirement accounts instead of a taxable account anyway. That retirement account not only provides for tax-protected growth like a whole life policy, but also a tax-rate arbitrage between your marginal rate at contribution and your effective rate at withdrawal, further boosting returns.

Even if your only choice is between buying bonds in a taxable account and buying whole life insurance, keep in mind that even at today's low interest rates you can still buy Vanguard's Long-Term Tax Exempt Muni Fund yielding 3.17% [2014] . The guaranteed return on whole life insurance cash value, held until your life expectancy, is about 2% and the projected return is only ~5%. Realistically, you should probably expect a return of 3%-4% over the long term on that policy. Of course, if you actually wish to cash out of that policy instead of borrowing from it (and paying interest for the right to borrow your own money), the earnings are just as taxable as any taxable bond fund. And if you want your money in a mere 10-20 years, you're going to come out way behind with the life insurance.

Now, if you really understand how whole life insurance works and you think its unique features outweigh its significant downsides, then feel free to run out and purchase as much as you like. It truly does not bother me. I do not make any money if you buy whole life, nor if you decide to buy something else. However, if you are like most, once you understand it, you won't buy it and in fact, if you already have, you'll probably be looking for the best way to get out of whole life insurance. Don't feel bad. 80% of those who purchase these policies surrender them prior to death, 36% within just five years. You've got to ask yourself why so many people who were apparently intending to hold this product for the next 40 or 50 years suddenly changed their mind. I'm sure it has nothing to do with it being inappropriately sold to the financially unsophisticated by insurance agents facing a terrible financial conflict of interest with their clients. Whole life insurance is a product made to be sold, not bought. It is a solution looking for a problem that exists for very few, if it exists at all.

Myth #24 — Whole Life Insurance Keeps Assets Off the FAFSA

This is one is merely misleading. The statement as it stands is true. The Free Application for Federal Student Aid (FAFSA) does NOT consider whole life insurance cash value as an asset of the student or the parents. The problem is, for the typical reader of this blog, that it doesn't matter. Your income alone will keep your child from qualifying for any need-based college financial aid. So if you buy a whole life policy for this reason, you're likely to be disappointed.

Myth #25 — Term Life Expires Without Paying Anything

Another misleading argument. I'm always surprised to see people fall for this line, but they do. Do you complain when you don't get to use your car insurance for any given six month period? How about when your house doesn't burn down? Or you don't get cancer and get to use your health insurance? Then why in the world would you complain that your term life insurance expires and you're still alive. Term life insurance is pure insurance. If you die, it pays. If you live, it doesn't. As a general rule, since on average insurance must cost more than it pays out (since insurance companies have both expenses and profits), you should insure against financial catastrophes. When it comes to death, the financial catastrophe is dying during your earning years, before you become financially independent. So that's the only time period you need to insure against. Some people only fall halfway for this argument, and buy return of premium term life insurance. The same principle applies, of course. You don't walk away empty-handed when your term life policy expires. You had insurance for the entire term, which is exactly what you needed.

Myth #26 — Whole Life Insurance Is the Perfect Investment

This outright lie comes from the true believers. They argue that whole life insurance is safe, liquid, tax-advantaged, creditor-proof, and offers a competitive return. These half-truths all add up to one big lie. Let's take them one at a time:

#1 Safe

Safe from the cash value going down, perhaps, but not safe from losing money. A huge percentage of whole life insurance purchasers lose money because they cancel the policy at some point in the first 5-15 years before they break even on their “investment.”

#2 Liquid

I guess it's more liquid than owning a website or a rental property, but it pales in comparison to the liquidity available in a savings account or a mutual fund that can be liquidated any day the market is open. Even inside retirement accounts, there is absolute liquidity after age 59 1/2, and fair liquidity even prior to that date. Most of the time with whole life insurance you don't even get your money, you just have the right to borrow against it at pre-set terms. You can get that with a HELOC.

#3 Tax-Advantaged

Few understand just how minor the tax advantages of whole life insurance are. There is no up-front deduction like a 401(k). Unlike a real investment, there are no capital gains rates if you surrender a policy with a gain and you cannot deduct the loss if you surrender it with a loss (the usual case). You don't get to use depreciation to reduce the tax burden of your income like with real estate. Instead of being able to withdraw the money tax-free like with a Roth IRA, you can only borrow against the policy, and that's tax-free but not interest-free, just like borrowing against your house, car, or mutual fund portfolio. Sure, you don't pay taxes on the “dividends,” but that's because they're actually a return of premium (i.e., you paid too much for the insurance). The only real tax break associated with life insurance is that the death benefit is tax-free. But that isn't any different from any other investment, where you get the step-up in basis at death. In addition, whole life can't be stretched like an IRA. The tax benefits, such as they are, are limited to a single generation.

#4 Creditor-Proof

Too few docs understand just how low the risk of needing this protection actually is. I calculate my risk of being successfully sued for an amount above policy limits at 1 in 10,000 per year. Maybe half that now that I'm practicing half-time. So should I be so unlucky as to be that one person, I would declare bankruptcy and be left only with protected assets. In my state, that's my retirement accounts, my spouse's assets, $40,000 in home equity, and whole life insurance cash value. Your state may or may not protect whole life insurance cash value. Please actually check if you are so paranoid to actually buy whole life insurance for this reason.

#5 Competitive Return

Are you kidding me? Competitive with what? Whole life insurance generally has a negative return for 5-15 years (sometimes more than 30 for really terrible policies). Even a good policy held for 5+ decades only guarantees a 2% return and projects a 5% return.

If I were going to draw up the perfect investment, it would definitely avoid the following characteristics of whole life insurance

- Guaranteed negative return for years

- Requirement to interact with and pay a commission to an insurance agent

- Requirement to give samples of body fluids and submit to a medical exam

- Requirement to answer pesky questions about my health

- Requirement to avoid risky activities

- Requirement to pay interest in order to use my own money

It only qualifies as an “okay” investment in certain very limited situations. It's not even close to a perfect one.

Myth #27 — Insurance Agents Are Just People

This is one of my favorites to see in any sort of discussion with an insurance agent about the merits of whole life insurance. It usually comes when I point out that my problem with whole life insurance isn't so much the product as the way in which it is sold. Obviously, many of them take that quite personally since they've dedicated their life and career to selling this product inappropriately. So they point out that there are bad doctors or that insurance agents are just people trying to make a living. I don't have a problem with the sales profession. I don't even have a problem with people earning commissions for selling stuff. Cindy gets paid on commission to sell ads right here at The White Coat Investor. But if you seek advice from Cindy about whether buying an ad at The White Coat Investor is a good idea for you, you're a fool. Insurance agents are just people and people respond to incentives. An insurance agent has a huge incentive to sell you a whole life policy. The commission on a policy is 50%-110% of the first year's premium. Now you know why he's trying so hard to sell you a big fat doctor policy.

Myth #28 — No 1099 Income with Whole Life

This was a new one to me. I thought I had heard every possible argument for buying a whole life policy until someone whipped this one out. How much trouble is it for you to deal with a 1099? It takes me about 30 seconds using Turbotax. Certainly not a reason to favor one investment over another. Remember not to let the tax tail wag the investment dog. Your goal isn't to minimize your taxes or maximize your tax-free income. It's to have the most money AFTER paying the taxes due.

Myth #29 — What Does The White Coat Investor Know? He's Just a Doctor, and Probably a Crappy One

Sometimes agents start with this argument, but frequently this is where they end, with ad hominem attacks. Sometimes it's phrased like one of these:

So, exactly how does being an ER doctor qualify you to give financial and insurance related advice?

Do everyone a favor and stick to studying medicine.

You’re young, a doctor and absolutely sure that you know everything.

Obviously, medicine has lots of problems and doctors don't know everything, but if the agent's best argument for whole life insurance is an ad hominem attack, that's a good sign that you should have stood up and walked out a long time ago.

Myth #30 — After Maxing Out a 401(k) and Roth IRA, Isn't Whole Life Insurance the Only Tax-Sheltered Option Left?

This is the wrong question to be asking, but the answer to it is still no. Just because it is the only option presented to you by an insurance agent, doesn't mean it is the only option. Other options for retirement savings include defined benefit/cash balance plans, an individual 401(k) for self-employment income, a spousal Roth IRA, your spouse's employer-provided accounts, and Health Savings Accounts (HSAs). In some ways doing Roth conversions and paying off debt is also tax-sheltered. But most importantly, there is no limit on investing in a non-qualified mutual fund account (where long-term gains and qualified dividends are somewhat sheltered from taxes) or in real estate (where income is sheltered by depreciation and capital gains can be deferred indefinitely by exchanging).

Obviously investing in whole life insurance compares better to investing in a taxable account than to a retirement account (where there is no comparison from a tax, investing, or in most states an asset protection standpoint). But the real problem with this argument is that it is focused entirely on the idea that any tax-advantaged investment is always better than any fully taxable investment. That simply isn't true. It also mixes up the idea of an investment and an account, two things that financially naïve doctors sometimes have a hard time telling apart. (Think of the accounts as different types of luggage and the investments as different types of clothing.) The real question to ask yourself when you hear this argument is “Where should I invest after maxing out my available retirement accounts?” The answer is a taxable, non-qualified account. Now you're left with the question of what long-term investment to invest in—tax-efficient mutual funds, real estate, or whole life insurance? It's pretty hard to really compare the merits of those three investments and end up choosing whole life insurance given its limitations and terrible returns previously discussed.

Myth #31 — The Estate Tax Exemption Could Go Down

The idea behind this argument is a rebuttal to the argument discussed in Myth #8. In summary, that argument is that you need whole life to avoid estate taxes, which is silly given the vast majority of doctors won't owe any federal estate taxes. The next step is for the agent to argue “Well, the estate tax exemption might be decreased.” Well, I suppose that's true. Congress can change any law they want any time they want. But buying insurance or investing based on what could happen seems foolhardy. I mean, it is probably just as likely that the estate tax is eliminated as the exemption reduced. It seems to me the best way to plan for the future is to project current law forward, since most laws aren't going to be significantly changed. If they are, you can make changes at that point. At any rate, it isn't like whole life insurance is some magic panacea to eliminate estate taxes. The only reason whole life insurance reduces your estate taxes is by making sure you have less money due to its low returns! The thing that reduces the size of your estate is the irrevocable trust you put the insurance into, and you don't even have to put insurance into it if you don't want to.

Myth #32 — Whole Life Insurance Protects from Nursing Home Creditors

This one was particularly fun to debunk. Apparently, the idea here is to not pay for your own nursing home care somehow by purchasing whole life insurance instead of mutual funds. I'm not sure exactly how those envisioning this process think it will go. Maybe they think the nursing home doesn't ask for money until after you die or something, which is, of course, completely silly. But I think what they're referring to is the ability to spend down your assets to Medicaid levels, get Medicaid to pay for the nursing home, and still be able to leave a huge inheritance to your heirs because Medicaid somehow doesn't look at the value of your whole life insurance.

The whole process of Medicaid planning is a little distasteful to me to be honest. The idea is to hide someone's assets from the state so that the heirs can have them, foisting the cost of caring for the owner of those assets on to the public. But even assuming that you have no ethical problem with doing this, it's unlikely to work very well. Medicaid is state law, so it varies by state, but in Utah, a person can have up to $2,000 in countable assets and still qualify for Medicaid. Above that level, no Medicaid until you spend down to that level. If there is a spouse, the spouse can keep 100% of assets up to $24,720 and 50% of assets up to $123,600. Above that, Medicaid won't pay for the nursing home. Non-countable assets in Utah include:

- Your home if your spouse lives in it

- The value of one vehicle (including a Tesla)

- Funds set aside for a funeral

- Household and personal items

- Cash value of your life insurance policies IF the total face value of all policies is <$1500

So I guess if you want to hide money from Medicaid in Utah, then you could go buy a $1,000 whole life policy. Most states have similar policies regarding cash value life insurance. Even if there were a state with a higher limit than Utah, this seems silly for someone who should spend her entire retirement as a multimillionaire to be making plans to spend down to Medicaid levels for nursing home care. A far better plan to stiff your fellow Utah taxpayer (assuming you have a spouse who doesn't need care) is to upgrade your house and your car.

Myth #33 — WCI Doesn't Understand the Opportunity Cost of Borrowing Against Whole Life Insurance and Investing Elsewhere

This statement has been made without explanation, but the idea isn't that complicated (nor misunderstood by WCI). You can borrow against the cash value in your whole life policy and use that money for whatever you want. You can spend it or you can invest it. Lots of whole life fans use fun phrases like “velocity of money” to describe buying a whole life policy, borrowing the money out, and investing it in something else. The really talented salesmen get you to invest it (along with any home equity they can get you to borrow out) in yet another insurance product.

Is there a cost to not maximally leveraging your life in this manner? Sure, anytime you can borrow at a lower rate and earn at a higher rate you'll come out ahead. But leverage works both ways, and the risk is not insignificant. What is not often mentioned by those advocating doing this is the opportunity cost of plunking money into a low return life insurance policy and buying unneeded death benefit instead of a higher returning investment. For instance, consider two options. You can invest $10K a year into an investment that returns 10% per year or you can buy a whole life policy that won't break even for 10 years. After 10 years, the first investment is worth $175K and the whole life policy only has a cash value of $100K. That's a $75K opportunity cost that apparently the “insurance agent doesn't understand.”

With a properly structured policy, you can break even in perhaps five years (maximizing the use of Paid-Up Additions), and using the combination of wash loans (interest rate to borrow against the policy =dividend rate of the policy) and a non-direct recognition policy, this idea becomes “not terrible.” You still have the opportunity cost of the first few years in the policy, but that is balanced out by a higher return on your cash in later years. I have discussed “Bank on Yourself” or “Infinite Banking” previously in detail if you are interested. It's not an insane use of whole life insurance, but it isn't for me. If you really understand how it works (it's going to take working through a lot of hype to do so) and want to do it, go for it.

Myth #34 — Buy Whole Life Insurance for the Long Term Care Rider

In recent years, insurance companies are adding on a Long Term Care rider to whole life insurance policies (and universal life policies and annuities) and agents are using the fear of expensive long term care to sell them. I find this appalling. Not only are you mixing insurance and investing, but you're now combining two different types of insurance policies with investing. Given the track record of insurance companies with long term care, I think most of my readers should strive to get a place where they can self-insure the risk of long term care, but even if they cannot, I'd prefer a simpler long term care policy on its own than mixing it with an otherwise unnecessary and expensive insurance policy.

The benefit of buying this as a rider of a whole life policy is that the premiums of the policy are guaranteed—you don't have the risk of the insurer upping the premiums like you do with a long term care policy or upping the cost of the underlying insurance like you do with a universal life policy. Those guarantees are worth something.

Remember we're not talking about just an accelerated death benefit. This is just another way of self-insuring long-term care, but with a lower return on the investments used to pay for it. You're really buying two policies combined into one. But there's no free lunch here. You're either paying more for the combined policy, or you're getting less of something, usually death benefit. Most likely, you're also paying for a life insurance policy you don't need or wouldn't otherwise buy. That death benefit isn't free. The reason life insurance companies stopped selling long term care insurance and started selling these hybrid policies is that their actuaries were convinced they are more likely to make money that way. That profit has to come from you, there is no other possible source.

If you do decide you wish to purchase some sort of long term care insurance policy, it is entirely possible that a hybrid product is right for you, but just like health and disability insurance, the devil is in the details. Read the fine print and be sure you know what guarantees the insurance company is actually providing. Know about what is covered, what isn't covered, and whether benefits are indexed to inflation or capped. Or better yet, live like a resident for 2-5 years out of residency so you'll be rich enough to self-insure this risk and never have to make this decision.

Myth #35 — We Don't Say Put All Your Money into Whole Life Insurance

This argument is simply bizarre, but used by agents once the prospective buyer has refused to buy the massive policy they were offered at first. A small commission is better than no commission, I guess. Of course, you shouldn't put all your money into whole life insurance, that's a straw man argument. Also, if buying a policy is a bad idea, you're going to be better off if you buy a small one than a big one. But that's hardly a reason to buy a policy in the first place. Like any asset class, if it isn't a good idea to put a significant chunk of your portfolio into it, it probably isn't a good idea to put any of your money into it.

Myth #36 — Yes, We Have a Few Bad Eggs But Most of Us Are Ethical

This argument is used when I point out that literally hundreds or even thousands of my readers have been sold clearly inappropriate insurance policies. The problem is there are two options to explain this phenomenon. The first is that these agents are unethical. The second is that they're incompetent. Given the statistic that 80% of policies are surrendered prior to death and 76% of the docs I've surveyed regret their purchase, this is hardly just a “Few Bad Eggs” doing this. It's an industry-wide problem.

Myth #37 — You Should Buy Insurance to Preserve Insurability

This one is used to sell insurance to people that don't even have a need for insurance. The idea is to prey upon their fear of the combined risk of needing insurance AND not being able to purchase it. One example would be a 25-year-old single doc with no kids. No life insurance need here. “But what if you get diabetes before you get married and have kids? You should buy the policy now.” Uhhhh . . .não.

First, you may never have dependents.

Second, if you do need it, you'll probably be able to buy it at that time at a reasonable price.

Third, if you do become less insurable, you will still likely have options for some insurance through an employer or other groups.

Fourth, even if you become uninsurable through anyone, the risks must be multiplied. For example, let's say there's a 5% risk of you becoming uninsurable before you have a real insurance need. And the risk of you dying before reaching financial independence is 5%. To get your true risk of a financial catastrophe, you must multiple those risks. 5% x 5% =0.25%. That is a 1 in 400 chance. Life is risky. You can't eliminate every possibility of something bad happening to you and even if you could, that wouldn't be a wise use of your money. Wait to buy insurance until you have a need for that insurance.

This argument is often even extended to children. If you're buying life insurance from the same company that sells you baby food, you're probably doing something wrong. Now, if you could buy a lot of future insurability for that kid very, very cheaply, that might be something to consider. Unfortunately, you can't really do that for several reasons:

First, you have to actually buy unneeded insurance. That newborn likely won't have any need at all for life insurance for 25-30 years.

Second, you're not pre-buying the policy that kid will need. You can't buy the right to buy a 30-year level term policy at age 30. You have to buy a whole life insurance policy. Which means you're also paying for insurance that will be unnecessary on the far end of life too, after the kid has become financially independent.

Third, you generally can't buy enough insurance, or even enough future insurability, to actually meet any sort of realistic life insurance need. Most of these infant policies are only $10K or so. That's basically a burial policy, and as sad as it would be to bury your kid, it's not a financial risk my readers should need to insure against. (I've even heard the argument that you should buy the policy so you can take a few months off work because you'll be too distraught to work, but that's what an emergency fund is for.) Even if you find a policy that allows you to purchase future insurability for a larger policy, let's say $500K, that's not going to mean much in 30 years when the life insurance need actually shows up for the first time, much less in 50 years when the kid is actually reasonably likely to die. At 3% inflation, $500K today will only be worth $200K in 30 years and $109K in 50 years. Better than nothing, but you went to all this effort and expense to preserve insurability and your kid still ended up with inadequate life insurance coverage.

Myth #38 — Whole Life Insurance Is a Great Investment to Put in Your Defined Benefit/Cash Balance Plan

I had this one pitched to me by a doc turned financial advisor of all people. The argument was that you could buy whole life with pre-tax dollars and then if you wanted to pull the policy out of the defined benefit plan you could do so. He felt this was an “advanced technique” for “high net worth folks.” I was flabbergasted. It was such a stupid idea I couldn't believe it. A defined benefit/cash balance plan already provides tax protected growth and asset protection, two reasons frequently cited to buy whole life insurance. You're now paying twice for those benefits. To make matters worse, should you die while this policy is in the defined benefit plan, part of the death benefit becomes taxable, negating another usual advantage of life insurance—a completely tax-free death benefit. But the main reason why this is such a stupid idea is when it comes time to close the defined benefit plan, which is usually done every 5-10 years or so in order to roll it into an IRA. At that point, you have to do one of two things.

First, you can surrender the policy and move the cash surrender value into the IRA. But what is the investment return on the first 5-10 years of a whole life policy? You break even if you're lucky. Not exactly a great investment for that time period, especially compared to a typical conservative mix of stocks and bonds.

Second, you can purchase the policy from the plan. Of course, you have to do that with AFTER-TAX dollars. So while you initially bought it with the pre-tax dollars in the plan, eventually you're going to have to cough up after-tax dollars for the policy. And then what are you left with? A whole life policy you probably neither want nor need and perhaps even with associated premiums you have to make each year. Some deal!

Myth #39 — More Money Is Passed Through Life Insurance

This myth showed up in a comment on a post on this blog. I thought it was particularly creative, especially with the way it was combined with Myth #8 (You Need Whole Life to Help For Estate Planning) and Myth #25 (Term Life Expires Without Paying Anything):

More money is passed through life insurance than any other way. I’ve seen too many people out live term which is throwing money away and need life insurance and are at that time in life uninsurable. Life is really used well in estate and trust planning.

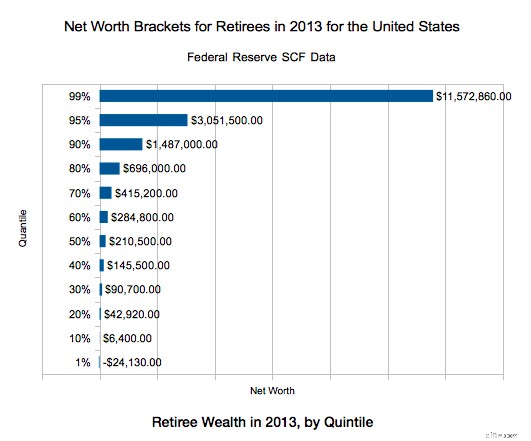

Surprisingly, this was the first time I had heard this argument. Being financially literate, of course I was able to immediately debunk it, but I suppose somebody might fall for it. There are two problems with this statement. First, it may not even be true. I looked and looked and looked for a study that showed what assets are actually inherited, without finding anything that actually quantified it. So if there is a study that actually says this, I suspect it is paid for by a life insurance company. Maybe it's true, maybe it's not, but I suspect it isn't given how few people have life insurance in force at their death. I suspect more money is left behind in houses than anything else. I mean, look at the net worth of people by age. Among retirees, the 50th percentile for net worth is $210K. That's got to be mostly house. The 80th percentile is $696K. That's about the average price of a house in my upper middle class neighborhood in a flyover state.

That jives with the average estate left behind at death:

- The average retired adult who dies in their 60s leaves behind $296K in net wealth,

- $313K in their 70s, $315K in their 80s

- $283K in their 90s

It seems very unlikely that the main inheritance most people receive is the proceeds of a life insurance policy given those numbers. How many retirees even carry life insurance? According to this, about 65% of those 65+. But 47% of those own less than $100K of life insurance. It is a well known statistic that fewer than 1% of term life insurance policies pay out. It isn't that the insurance companies aren't good for the money, it's just that people out live the term. A lesser known statistic is that 80%-90% of whole life insurance policies don't pay out either. They're surrendered prior to death, often at a loss since 1/3 of policies are surrendered in the first 5 years and over half in the first 10 years.

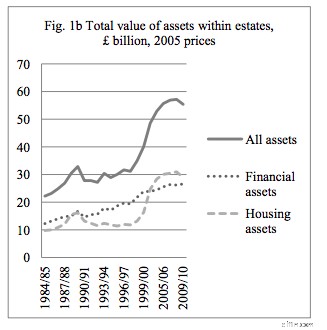

I did manage to find some UK data, however, which suggests my hunch (that people inherit more in real estate than life insurance proceeds) is correct.

As you can see, more than half of inherited assets are housing assets, so clearly more assets cannot be passed as life insurance than anything else.

Perhaps the agent wasn't referring to the median inheritance though. Perhaps he was referring to the total amount of dollars passed to heirs. I could find no data to support nor refute that notion.

Second, even if the statement is true, it is irrelevant. Given that THE PURPOSE of life insurance is to pass assets on to heirs, that's hardly an argument to buy life insurance for some reason besides the death benefit. As I've always said, if you want a life long death benefit that gradually increases throughout your life, then a whole life insurance policy is a great way to get that (although a guaranteed universal life policy can provide a level life long death benefit at about half the price and is probably a better solution for those who really need a permanent death benefit). Bear in mind that you are likely to leave a larger inheritance by investing in stocks and real estate than buying life insurance due to the higher returns, and those assets, just like life insurance, provide a tax-free inheritance to your heirs. Life insurance only provides a larger inheritance if you die well before your life expectancy.

Myth #40 — You Get an Investment and Life Insurance

This one confuses a lot of people and they get really mad when they realize how whole life insurance works. They mistakenly believe that they get a death benefit for their heirs AND a separate “cash value” investment type account that they can use themselves or leave for their heirs. What they do not realize is these two pots of money are one and the same. That which you use for yourself does not get passed on to your heirs. When they discover this fact, they feel like the insurance company is stealing a bunch of money from them and their heirs.

In reality, when you borrow against your life insurance policy, you are borrowing against your death benefit. When you die, your heirs get the death benefit minus any outstanding loans. The amount of the outstanding loans, of course, can never be more than the cash surrender value of the policy, which gradually grows to an amount very close to the death benefit at your life expectancy. So really the cash value just tells you how much of the death benefit you can borrow at any time. You can either borrow this pot of money (death benefit/cash value/surrender value) and spend it yourself, surrender the policy and spend the money, die and leave the money to your heirs, or some combination of the above. But there isn't two pots of money. There isn't a $400K cash value and a $1M death benefit. There is just a $1M death benefit. If you spend $400K of it, your heirs only get $600K of it. So you don't get an investment AND life insurance, you get an investment OR life insurance.

Summing It Up

Aí está. Forty reasons for buying whole life insurance debunked. Não se preocupe; the agents who sell this stuff will come up with more. Just hang out in the comments section over the next year or two and you can watch. Whole life insurance is a product designed to be sold, not bought and the only way to win an argument with an agent trying to sell it to you is to stand up and walk away. As Upton Sinclair famously said, “It is difficult to get a man to understand something, when his salary depends on his not understanding it.” Maybe it should be called Whole LIE Insurance.

Whole life insurance is a terrible investment if you don't hold on to it to your death. Since the vast majority of people surrender their policies prior to death, it is a terrible investment for the vast majority of those who purchase it. If you want to invest in it, then you need to place a very high value on its unique aspects and not mind it's serious downsides.

The ideal purchaser of whole life insurance should:

- Need or desire a guaranteed, but possibly slowly increasing, life-long death benefit,

- Understand that the guarantee/contract essentially relies on the insurance company staying in business for as long as he lives for any policy of reasonable size,

- Live in a state that protects 100% of the cash value from creditors,

- Have some estate planning liquidity issues,

- Be in excellent health,

- Pursue no dangerous hobbies,

- Not mind having low returns on his investment despite holding it for decades,

- Have serious philosophical aversion to using traditional financing resources such as banks and credit unions (or simply just saving up for what you want to buy),

- Have already maxed out all available retirement accounts including backdoor Roth IRAs and HSAs, and

- Be willing to hold on to the policy until death no matter what changes in his financial life in the future.

The fact is that only a tiny percentage of the population, far smaller than the number of people who have been sold these policies historically, meets all or even most of these criteria. Whole life insurance remains a product designed to be sold, not bought.

Have more questions about life insurance and what kind of policies would be best for you? Hire a WCI-vetted professional to help you sort it out.

Agree? Disagree? Please reference which “myth” you're referring to in your comment and keep comments civil and on topic. Ad hominem attacks will be deleted.

[This updated post was originally published as a series from 2013-2019.]

The White Coat Investor may receive compensation from White Coat Insurance Services, LLC; licensed in all states including MA and DC; CA license #6009217; NY license #1758759 (exp. 6/2027); Registered address:10610 S. Jordan Gateway, #200 South Jordan, UT 84095. This does not affect the cost or coverage of insurance.

-

3 razões pelas quais você precisa de uma câmera de painel em seu carro

Aqui estão as principais razões para comprar uma câmera de painel, além de recursos-chave para procurar. (iStock) Nos últimos anos, as câmeras do painel se tornaram uma compra cada vez mais popular

-

Precisa de dinheiro para passar as férias? Aqui estão 16 empresas que procuram ajuda sazonal

Muitos ou todos os produtos aqui são de nossos parceiros que nos pagam uma comissão. É assim que ganhamos dinheiro. Mas nossa integridade editorial garante que as opiniões de nossos especialistas não

Artigos em Destaque

- Vivendo do Groupon:Chicago Man tenta desafio de um ano por US$ 100.000

- Se você quiser comprar uma casa em 2019,

- Você pode refinanciar uma hipoteca com crédito ruim?

- O que é uma conta de apropriação?

- Como evitar tomar decisões precipitadas em sua carreira

- 4 estratégias comprovadas para economizar dinheiro em 2024 | Abeto

- Entretenimento econômico:4 ideias para diversão acessível

- Melhores bancos nacionais dos EUA em 2021

-

Como realizar uma análise de lucro por volume de custo (CVP)

Como realizar uma análise de lucro por volume de custo (CVP) A análise de lucro por volume de custo ajuda os empresários a verem os custos de seus produtos sob uma nova luz. Siga estas etapas na próxima vez que precisar precificar um produto ou criar uma meta d...

-

O que são ativos líquidos irrestritos?

O que são ativos líquidos irrestritos? p Ativos líquidos irrestritos são as doações de ativos (atuais e / ou fixas) feitas a organizações sem fins lucrativos (NPOs) Organizações sem fins lucrativos Uma organização sem fins lucrativos conce...